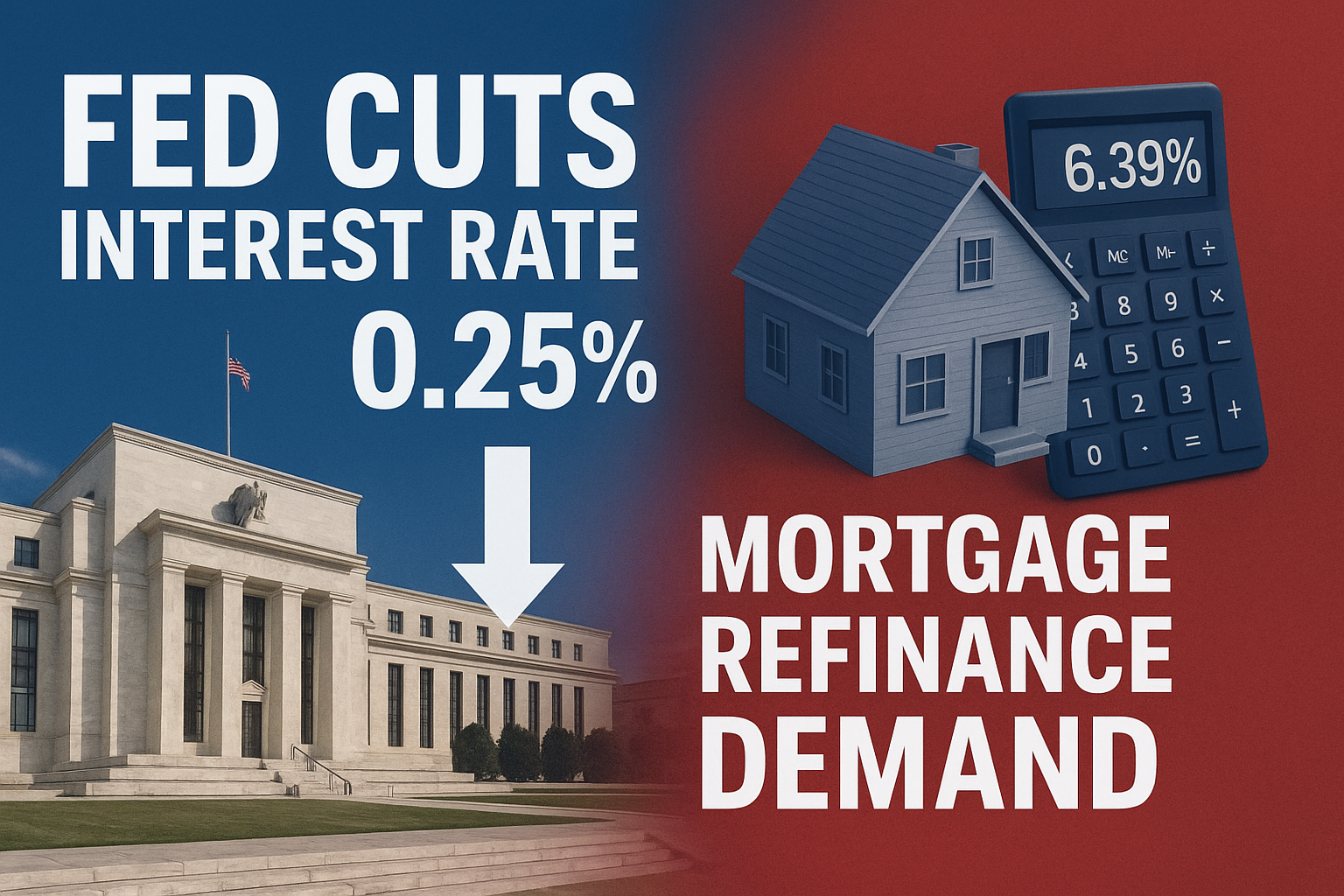

On September 17, 2025, the Federal Reserve reduced its benchmark interest rate by 0.25 percentage points, setting a new target range of 4.00% to 4.25% for mortgage.

This marked the Fed’s first cut since December 2024, and officials cited slowing job growth, rising unemployment risks, and lingering inflation pressures as reasons for the move. Chair Jerome Powell described the cut as a “risk-management step” to balance economic slowdown with still-elevated inflation.

Notably, Fed board member Stephen Miran dissented, pushing for a deeper half-point cut. The Fed also signaled that more reductions are likely before the end of the year.

Why Mortgage Borrowers Are Celebrating

The immediate impact of the Fed’s decision rippled into the housing sector. According to CNBC, U.S. mortgage refinance demand spiked nearly 60% in a single week as homeowners rushed to take advantage of lower borrowing costs.

Mortgage rates, which had climbed above 7% earlier in 2025, saw their sharpest drop in over a year. The decline revived interest among borrowers who had been sitting on the sidelines, particularly those with adjustable-rate mortgages and recent buyers who locked in high rates.

Read Also- ![]() Mark Zuckerberg unveils $799 Meta × Ray-Ban Display Glasses — stylish AR eyewear blending fashion + tech. #MetaRayBan #SmartGlasses #FutureOfTech

Mark Zuckerberg unveils $799 Meta × Ray-Ban Display Glasses — stylish AR eyewear blending fashion + tech. #MetaRayBan #SmartGlasses #FutureOfTech

Key Takeaways for Homeowners

-

Refinancing wave: Applications for mortgage refinancing rose nearly 60% week-over-week, the largest increase in years.

-

Lower monthly payments: Homeowners refinancing at current levels could save hundreds of dollars per month, depending on loan size.

-

Purchase market response: While refinancing drove the surge, mortgage applications for new home purchases also ticked up slightly.

-

Short-lived window? Economists caution that rates could remain volatile depending on inflation, labor market data, and Fed policy.

Broader Economic Implications

The Fed’s rate cut highlights the delicate balance between supporting the job market and containing inflation. By easing borrowing costs, the central bank hopes to prevent a deeper slowdown.

But the surge in refinancing also signals how quickly consumer behavior can shift. As households lower debt costs, they may spend more elsewhere, helping support broader economic activity.

At the same time, savers may see yields decline on high-interest accounts, CDs, and bonds. Investors will be watching closely as the Fed plots its next moves.

What to Watch Next

-

Future Fed cuts – Markets expect at least one more reduction before year-end.

-

Mortgage rate trends – Will lenders keep cutting, or will rates stabilize?

-

Housing affordability – Lower rates may boost demand, but limited inventory remains a challenge.

-

Labor market data – Job reports will heavily influence Fed policy in the months ahead.

FAQs

1. How much did the Fed cut rates in September 2025?

By 25 basis points (0.25%), bringing the target range to 4.00%–4.25%.

2. Why did mortgage refinancing demand surge?

Because mortgage rates dropped sharply following the Fed’s rate cut, creating an opportunity for borrowers to save on monthly payments.

3. Will mortgage rates keep falling?

Analysts expect some additional easing, but rates depend on inflation and Fed policy decisions.

4. Does refinancing make sense for everyone?

Not always—closing costs and loan terms matter. Borrowers should calculate long-term savings before refinancing.

5. Will there be more Fed rate cuts this year?

Yes, projections suggest at least one more cut if inflation remains manageable and the labor market continues to soften.